Latin America’s Energy Paradox: Clean Power in an Oil Economy

By: Lucia Piantini

Photo credits: The Rio Times

Latin America is often described as a quiet leader in the global energy transition, and in many ways, that is true. Nearly 63% of the region’s electricity already comes from renewable sources, far above the global average, thanks to decades of hydropower development and rapid growth in wind and solar energy. Countries like Brazil and Chile now generate most of their electricity from clean sources, and renewable energy auctions continue to expand capacity across the continent. On the surface, the region appears to be a climate success story.

But the deeper picture is more complicated. Oil still accounts for roughly 40% of Latin America’s primary energy supply, and fossil fuels make up close to 70% of total energy consumption. Energy demand itself is expected to grow by about 20% by 2060, meaning renewables are not simply replacing fossil fuels, but that both systems are expanding simultaneously. Brazil continues offshore drilling, Mexico supports its state-owned oil company, and hydrocarbon exports remain central to public revenues in several economies. For governments balancing fiscal stability and social spending, abandoning oil too quickly is not politically simple.

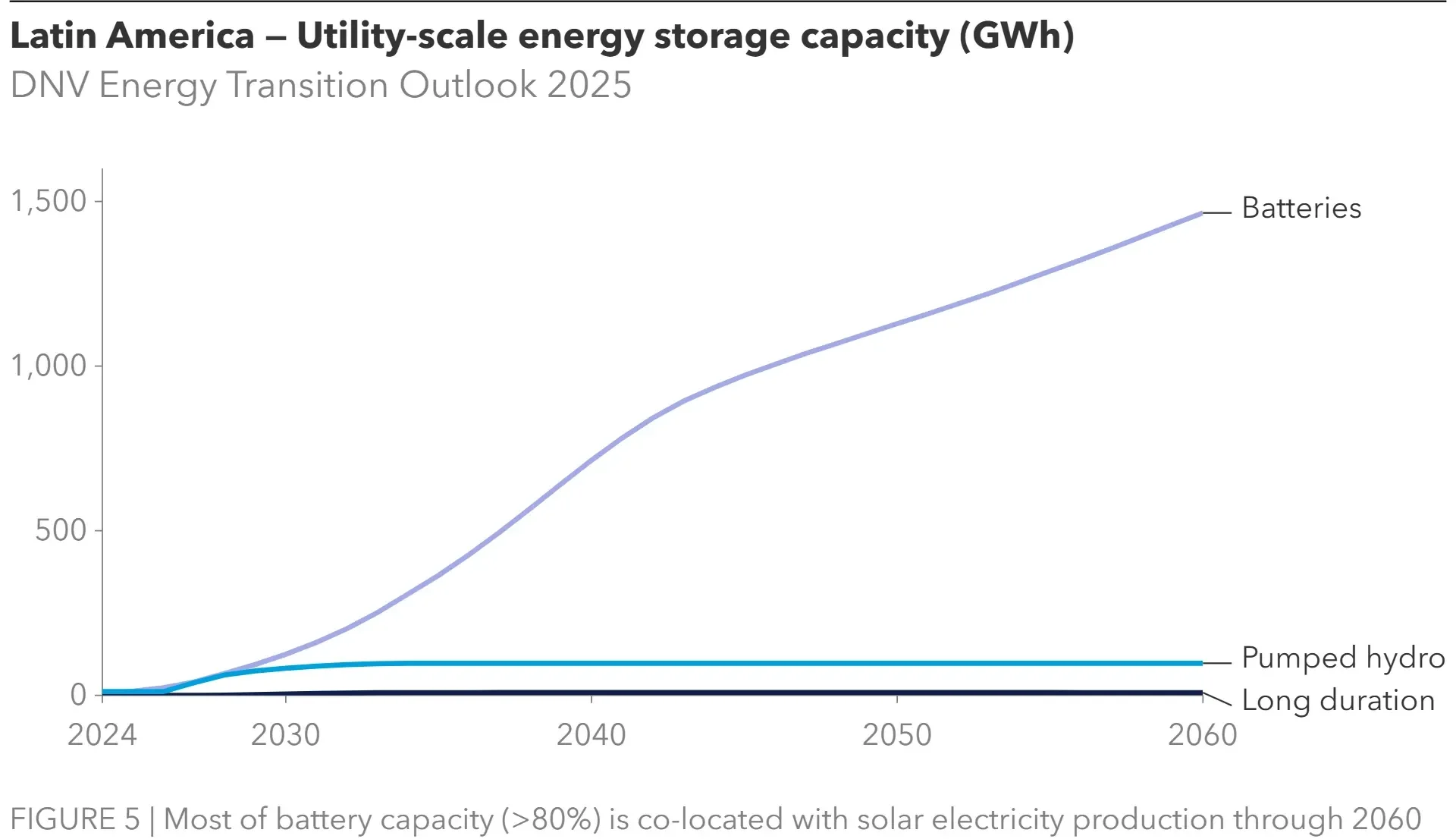

At the same time, investment in clean energy is accelerating. Chile is rapidly scaling battery storage to support renewable grids, and Brazil has committed funding to large green hydrogen projects aimed at positioning itself as a future exporter of clean fuels. Solar and wind are now among the cheapest sources of electricity in many Latin American markets. Yet transportation remains a weak point. While Brazil leads in biofuel blending, electric vehicle adoption across the region still lags far behind Europe and China.

The region’s biggest constraint may not be resources, but infrastructure. According to JPMorgan’s analysis on Latin America’s energy landscape, electricity demand is rising steadily, driven by urbanization, electrification, and industrial growth. In many countries, transmission networks and grid capacity have not expanded at the same pace as renewable generation. In Chile, for example, solar output has at times exceeded what the grid can absorb, forcing energy curtailment. The challenge is not a shortage of clean energy potential, but rather insufficient modernized infrastructure to distribute it efficiently.

Photo: Reuters

Bridging this gap will require substantial capital. Regional development banks estimate that hundreds of billions of dollars in investment will be needed this decade to upgrade grids, expand transmission lines, and integrate storage. Private capital has begun to respond, but whether infrastructure keeps pace with demand will shape the success of Latin America’s transition.

Lithium Extraction Site in Chile

Latin America may also hold one of the strongest strategic advantages in the global transition: minerals. Chile and Argentina possess some of the world’s largest lithium reserves, and Peru is a major copper producer, both of which are essential materials for batteries and renewable infrastructure. If managed effectively, these resources could allow the region to move beyond energy production and become central to clean technology supply chains. The region’s transition, therefore, is not dramatic or abrupt. It is pragmatic and uneven. Clean electricity is expanding quickly, but fossil fuels remain embedded in economic structures and political priorities. The real question is not whether Latin America is transitioning, but whether it can convert its natural advantages into lasting, sustainable growth without remaining structurally tied to oil dependency.